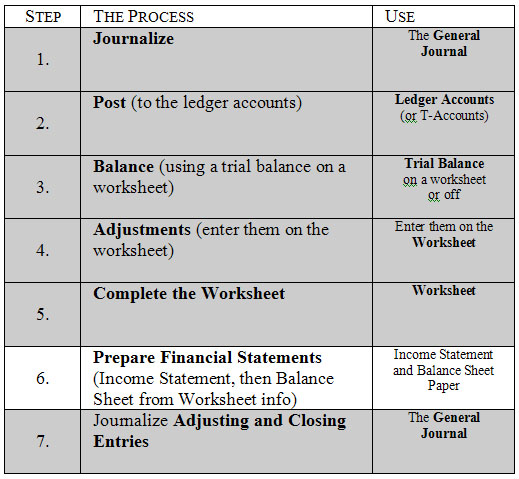

In this lesson we are changing the following step in

the accounting cycle:

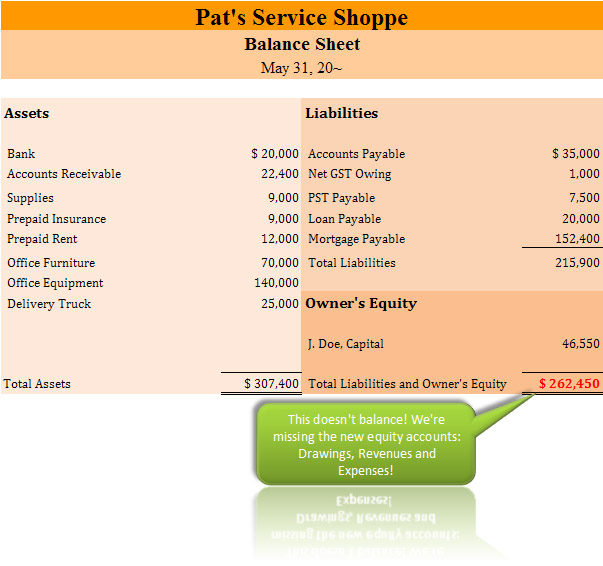

Thus far we have used a balance sheet that is arranged

in the same fashion as the accounting equation – that is, Assets on

the left, Liabilities and Equity on the right, just like the one shown below.

Our needs however, have surpassed this simple format.

There are three major reasons:

We have several contra-accounts that we need to

show and sub-total on the balance sheet. This requires a balance sheet

with multiple columns

As we begin to require more specific information

for analysis and reporting, we need to categorize, and classify certain

accounts into particular groups.

Lastly, we can’t balance anymore using

the old method! Remember the “Capital” account is the balance

from the beginning of the period. All changes to Owner’s Equity

have been channelled into the Drawings, Revenue, and Expense accounts

and thus are missing from Capital. (If you recall, this

is why we had to transfer the net income number on the worksheet at

the bottom click here

to review).

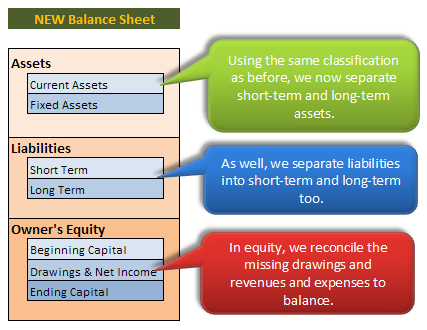

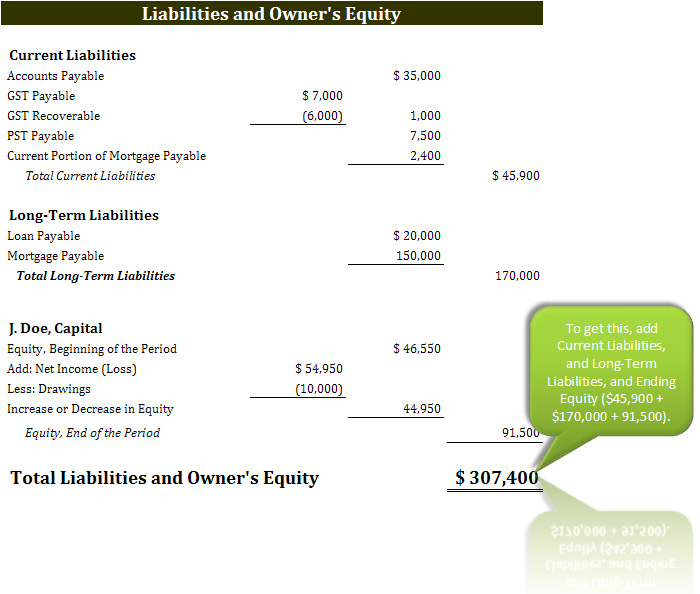

Though you may be aware of the classification of short-term

and long-term assets and liabilities, now we physically show them as separate

on the Balance Sheet. The presentation breaks down as follows:

Now that you know classification and column use, we

will begin to construct a New Classified

Balance Sheet section by section before we cover item 4, which is the

equity section.

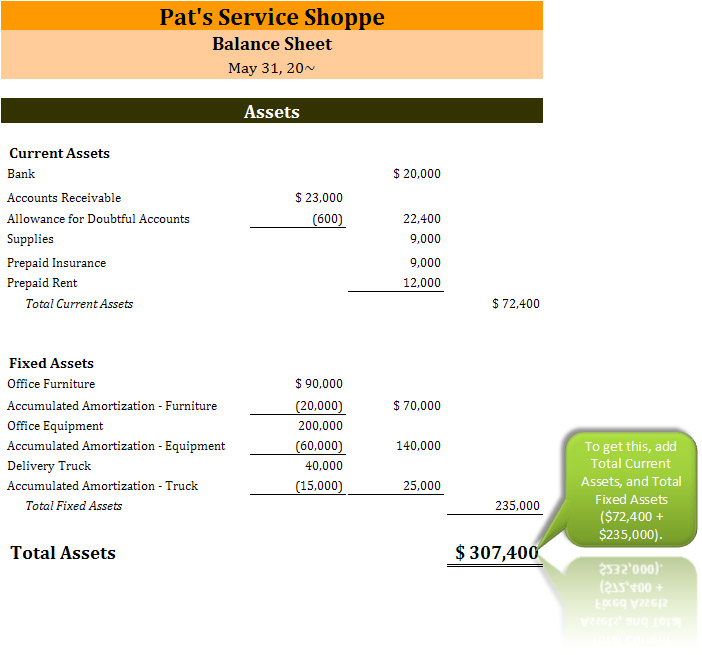

The first section is Assets. Remember this is divided

into short-term and long-term assets. Short term assets are called Current

Assets. We have one contra

account to deal with here; it is the Allowance for doubtful accounts

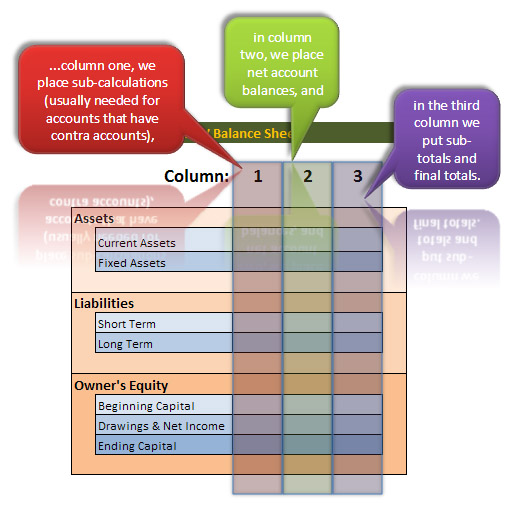

Soon you will have to perform financial analysis on

the Balance Sheets and Income Statements of companies.

By classifying the accounts on a Balance Sheet, this

analysis becomes much, much easier. It will allow you to quickly find and

calculate numbers that you will require.

Click on the arrows in the middle of the Balance Sheet

we just finished below to see how:

{kind=link}