Knowledge - Multiple Choice (1 mark

each)

Identify the best choice that best completes the statement or answers

the question.

You may wish to use this tool

to help you answer some of the questions.

|

|

|

1.

|

Marginal revenue (MR) may be defined as

the:

a. | change in average revenue associated with the sale of one more

unit of output | b. | change in product price

associated with the sale of one more unit of output | c. | change in total revenue associated with the sale of one more unit of

output | d. | difference between product price and average

cost |

|

|

|

2.

|

Fixed costs (AFC) per unit:

a. | Are not influenced by production

levels | b. | Do not vary | c. | Will continuously fall as

more and more is produced | d. | Are items like labour,

materials, and taxes |

|

|

|

3.

|

Which of the following is true?

a. | A firm’s total cost (TC) will not always rise with

production | b. | A firm’t total

variable costs (TVC) will fall at first, but then rise as more and more is

produced. | c. | Total costs per unit (ATC) have a minimum level, because variable

costs will fall then rise. | d. | Total cost per unit (ATC)

will continuously fall as more is produced and a firm benefits from economies of

scale |

|

|

|

4.

|

The behaviour of a firm’s average variable cost curve

(AVC) is explained by:

a. | Economies of scale | b. | Law of supply and demand | c. | None of these is

correct | d. | Economies of scale, then diminishing

returns |

|

|

|

5.

|

If a business in a perfectly competitive industry is

confronted with a price of $5, its marginal revenue:

a. | may be either greater or less than $5 | b. | will be less than $5 | c. | will also be

$5 | d. | will be greater than $5 |

|

|

|

6.

|

The profit-maximizing rule of producing to where MR=MC

applies:

a. | only to perfectly competitive

businesses | b. | to businesses in all types

of industries | c. | only when the business is a

"price-taker", and can’t influence the price at all | d. | only to monopolies |

|

|

|

7.

|

A perfectly competitive business' demand curve

is a:

a. | straight line parallel to the quantity

axis | b. | upward-sloping straight line reflecting the constant value of

price as output increases | c. | straight line parallel to

the price axis | d. | downward-sloping straight

line reflecting the law of demand |

|

|

|

8.

|

A perfectly competitive business reaches its lowest

possible breakeven point where:

a. | normal profits are zero | b. | price equals average total cost | c. | the total revenue line

equals the average variable cost line | d. | marginal cost intersects

the average variable cost curve |

|

|

|

9.

|

Which of the following is a major limitation to the theory

of perfectly competitive markets?

a. | externalities usually don’t apply to small

businesses | b. | effeciency and a small

production scale often don’t co-exist | c. | perfectly competitive firms

don’t make any profit | d. | government involvement

limits the number of firms in most industries, in effect creating barriers to

entry |

|

|

|

10.

|

In the long run for a perfectly competitive firm, resources

are distributed in a way that maximizes the overall satisfaction of consumers and the efficient use

of resources when production occurs at the point at which:

a. | P=MC=ATC (price equals marginal cost) | b. | MC=AVC (marginal cost intersects average variable cost) | c. | P=AVC (price is equal to average variable cost) | d. | P=AR (price is equal to average revenue) |

|

|

|

11.

|

A monopolisticly competitive firm’s marginal revenue

curve is just like a monopoly’s in that it:

a. | is downward-sloping and lies below the demand

curve | b. | is downward-sloping and coincides with the demand

curve | c. | does not exist because the business is a

price-maker | d. | coincides with the demand

curve and is parallel to the horizontal axis

|

|

|

|

12.

|

A monopolisticly competitive firm maximizes short-run

profits by:

a. | setting price equal to marginal cost | b. | setting the price at the point where average revenue equals marginal

cost | c. | producing at the the quantity of output where marginal revenue

equals marginal cost | d. | equating demand and average

revenue |

|

|

|

13.

|

If an oligopolist is faced with a marginal revenue

curve that has a gap in it, we may assume that:

a. | none of these answers are correct. | b. | it is selling a differentiated product | c. | its demand curve is kinked | d. | it is colluding with its

rivals to maximize joint profits |

|

|

|

14.

|

The kinked demand curve indicates a situation in which an

oligopolist will be:

a. | eager to lower price | b. | eager to either raise or lower prices | c. | interested in maintaining the going price even as costs

change | d. | willing to raise price |

|

|

|

15.

|

Which one of the following is usually considered a societal

benefit of a monopoly?

a. | economies of scale | b. | price discrimination | c. | higher

profits | d. | the monopoly can control price through

supply |

|

|

|

16.

|

Because of the market conditions of a monopoly, it

can:

a. | get away with collusion | b. | choose both the quantity produced and the price consumers are willing to

pay | c. | form a perfectly competitive partnership to maximize

efficiency | d. | discriminate between market

segments and set separate prices for each to maximize profits |

|

|

|

17.

|

Which of the following market structures almost always

experiences some economic profits in the long-run?

a. | Perfect Competition | b. | Monopolistic Competition | c. | Oligopoly | d. | None of the

above |

|

|

|

18.

|

Which of the following is true about game

theory?

a. | The views of Adam Smith are correct and complete as they apply to

monopolistic markets | b. | In a monopolistic market

created by collusion, once the colluding equalibrium point is reached, firms have an incentive to

cheat | c. | Collusion (or cooperating) is not in the best interests of

individual firms in the long run, competition is better | d. | When firms collude society is better off |

|

|

|

19.

|

Which of the following is NOT a market condition for a

Monopoly?

a. | Many buyers | b. | Only one

seller | c. | No substitutes exist | d. | There are very few barriers to entry |

|

|

|

20.

|

Assume the XYZ Corporation is producing 20 units of

output. It is selling this output in a perfectly competitive market at $10 per unit. Its

fixed costs are $100 and its average variable cost is $3 at 20 units of output. On the basis of

this information we can say that the corporation is making TOTAL economic profits of how much

money?

a. | $97 | b. | $40 | c. | $140 | d. | $17 per

unit |

|

|

|

Below is revenue and cost data for a

monopoly:

Price

| Quantity

Produced | Total

Revenue |

Total

Cost

| 6.50 | 3.00 | 19.50 | 5.00 | 6.00 | 4.00 | 24.00 | 6.00 | 5.50 | 5.00 | 27.50 | 6.50 | 4.85 | 6.00 | 29.10 | 7.50 | 4.35 | 7.00 | 30.45 | 9.00 | 3.90 | 8.00 | 31.20 | 11.00 | 3.50 | 9.00 | 31.50 | 14.00 | | | | |

|

|

|

21.

|

The price for the monopoly at the point of maximum profit

will be:

a. | 6.50 | b. | 6.00 | c. | 5.50 | d. | 4.85 | e. | 4.35 | f. | 3.90 | g. | 3.50 |

|

|

|

22.

|

Using the same data for this monopoly, marginal revenue from

a price decrease from $6.00 to $5.50 is:

a. | $0.70 | b. | -$3.50 | c. |

$0.875 | d. | $3.50 | e. | None of these answers is

correct |

|

|

|

Total

Output | Price | Total Cost | Average

Cost | Marginal Cost | 0 | 20 | 13.5 | | | 1 | 19 | 17.5 | 17.50 | | 2 | 18 | 22 | 11.00 | | | | | | |

|

|

|

23.

|

Using the chart above, find the marginal cost from moving from one unit of

production to two.

a. | $6.50 | b. | 4.5 units | c. | $2.25 | d. | $4.50 |

|

|

|

24.

|

Using the chart above, find the marginal revenue from moving from one unit of

production to two.

|

|

|

Below is a graph for a perfectly competitive firm operating in the widget

market. The market graph is shown in the top right corner. Answer the questions that

follow.

Pop out this graph by clicking here.

|

|

|

25.

|

Which of the following is true about the state of the MARKET at point #1 in the

graph?

a. | It is the short run | b. | It is not at equilibrium | c. | There are barriers

to entry | d. | None of these answers is correct |

|

|

|

26.

|

Which of the following is true about the state of the FIRM at point #1 in the

graph?

a. | It is at equilibrium | b. | It is producing at the most efficient level of

production | c. | It is not maximizing profits | d. | It is earning economic

profits |

|

|

|

27.

|

Which of the following could be true about the state of the MARKET at point #2

in the graph?

a. | Firms have lowered their prices in the market | b. | New firms entered

the industry | c. | Consumer tastes and preferences changed | d. | The market

experienced a shortage |

|

|

|

28.

|

Which of the following could be true about the state of the FIRM at point #2 in

the graph?

a. | This firm lowered prices and the market followed | b. | This firm must shut

down to save money | c. | This firm should produce more to maximize

profit | d. | This firm is losing money, but not enough to shut

down |

|

|

|

29.

|

Which of the following could be true about the state of the MARKET at point #3

in the graph?

a. | The market demand has increased raising price levels | b. | Less efficient firms

reached their shut down point and left, raising market price | c. | Since no money is

being made, more firms will leave, raising market price further and profits will

return. | d. | None of these statements is true |

|

|

|

30.

|

Which of the following could be true about the state of the FIRM at point #3 in

the graph?

a. | This firm is making no economic profit but will eventually as this is the short

run | b. | This firm will eventually shut down since it’s not making

money | c. | This is the short run condition for this firm where it is still losing

money | d. | This firm is producing at its long-run maximum profit level of

output |

|

|

|

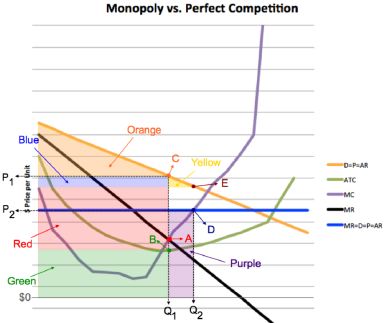

Ceteris paribus, The following graph is a comparison between a monopoly and a

perfectly competitive firm. NOTE: It assumes these two firms have the same cost structure.

Only revenue-related lines are different. Answer the questions that

follow.

Pop out this graph by clicking here.

|

|

|

31.

|

Does graph depict a comparison between a perfectly competitive firm and a

monopoly in the short run, or in the long run?

a. | Short Run | b. | Long Run | c. | Can’t be

determined |

|

|

|

32.

|

Which price level represents what the monopoly would sell this product

for?

|

|

|

33.

|

What is the quantity produced by the monopoly?

|

|

|

34.

|

Total revenue generated by the monopoly is the shaded area(s):

a. | Orange, Blue, Red, Green | b. | Blue, Red, Green | c. | Blue,

Red | d. | Green | e. | Green, Purple |

|

|

|

35.

|

Total revenue generated by the perfectly competitive firm is the area bounded by

the height by width of:

a. | P1 by Q1 | b. | P1 by Q2 | c. | P2 by

Q1 | d. | P2 by Q2 | e. | The answer is not

shown |

|

|

|

36.

|

The point of profit maximization for the monopoly occurs where its marginal

revenue equals its marginal cost. This occurs at the point:

|

|

|

37.

|

The point of profit maximization for the perfectly competitive firm occurs where

its marginal revenue equals its marginal cost. This occurs at the point:

|

|

|

38.

|

The cost per unit at maximum profit for the monopoly is the point:

|

|

|

39.

|

The cost per unit at maximum profit for the prefectly competitive firm is the

point:

a. | A | b. | B | c. | C | d. |

It is not shown. |

e. | E | f. |

D |

|

|

|

40.

|

The most efficient point of production for either firm is represented by the

point:

a. | A | b. | B | c. | C | d. | D | e. | E | f. | It is not

indicated. |

|

|

|

41.

|

The monopoly at maximum profit will set a price for its product that can be

found by looking at the following point on the its demand curve:

a. | A | b. | B | c. | C | d. | D | e. | E | f. | It is not

shown. |

|

|

|

42.

|

The perfectly competitive firm at maximum profit must accept a market price that

can be found by looking at the following point on the its demand curve:

|

|

|

43.

|

If the government forced the monopoly to produce at the point of maximum

long-run efficiency like the perfeclty competitive firm, what point on its demand curve would

represent this price and output level?

|

|

|

44.

|

Maximum total revenue for the monopoly occurs at:

a. | A point left of Q1 | b. | Q1 | c. | Between Q1 and

Q2 | d. | Q2 | e. | To the right of

Q2 |

|

|

|

45.

|

Total cost for the monopoly is represented by the shaded area:

a. | Green | b. | Red | c. | Blue | d. | Orange | e. | Yellow | f. | Purple | g. | Blue,

Red | h. | Blue, Red, Green |

|

|

|

46.

|

The consumer surplus for the monopoly is represented by the area

coloured:

a. | Orange | b. | Yellow | c. | Blue,

Red | d. | Orange, Blue, Yellow | e. | Can’t be

determined |

|

|

|

47.

|

If the monopoly was forced to produced at the sane level of output as the

competitive firm, then the consumer surplus would be represented by the area coloured:

a. | Orange | b. | Yellow | c. | Blue,

Red | d. | Orange, Blue, Yellow | e. | Can’t be

determined |

|